By: Nathan Rock

Introduction

Over the span of four years, Google co-founder Larry Page donated more than $400 million from his private foundation to charity. While this might seem incredibly generous, it was discovered that “none of [the] $400 million . . . was actually going directly to charities.”[1] Instead, Page’s foundation was directing the money into a charitable-giving fund, called a donor-advised fund (DAF), where the money could sit indefinitely.

A DAF is a giving vehicle that allows donors to “make a charitable contribution, receive an immediate tax deduction, and then recommend grants” over any period of time.[2] DAFs have become increasingly popular—in fact, Bill Ackman recently announced he donated $1.3 billion worth of Coupang stock to a DAF, in addition to one other nonprofit.[3]

DAFs are simple to set up and have made it easier for individuals to make philanthropic donations, but as Page’s foundation has shown, DAFs can be manipulated. Currently, over $141 billion sit in DAFs, with more money being put in each year.[4] Because DAFs have so much idle capital, many refer to DAFs as “zombie philanthropy.”[5]

It is time for the US government to intervene by changing regulations in order to unlock the $141 billion stuck in DAFs. US Congress should make the following changes:

- Place limitations on the tax-exempt status of DAF sponsors

- Create a dormant account program for DAFs

- Eliminate the ability for foundations to donate to DAFs

This article outlines the problems with DAFs and how each change should be implemented.

Zombie Philanthropy – Understanding the problem.

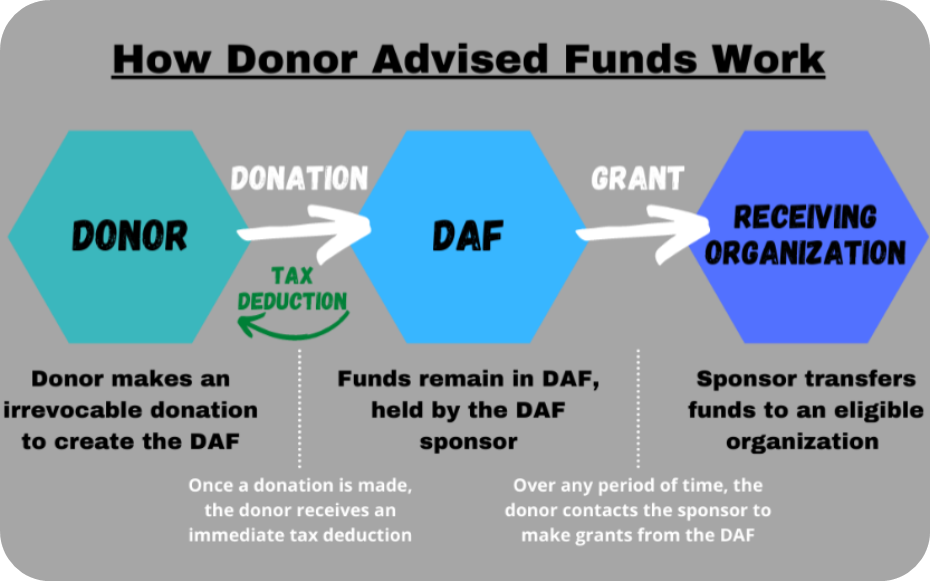

First, we need to understand how a DAF operates. Below is a diagram illustrating how money flows through a DAF.

It is important to understand the following:

- The donor immediately receives a tax deduction, and the donation is held by a sponsoring organization (DAF sponsor).

- The DAF is an individual account linked to the donor (i.e. the sponsor can host numerous DAFs, but it is not one pool of money). While waiting to be disbursed, the DAF is usually placed in an investment account.

- The sponsor maintains legal rights of the DAF while the donor acts as an “advisor,” making grant recommendations to charitable organizations. It is unlikely the sponsor would refuse the donor’s grant recommendation as long as the organization meets eligibility requirements.

- There is no legal requirement as to when the DAF balance must be distributed.

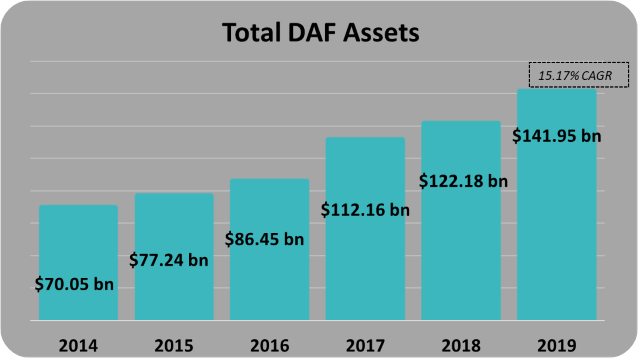

DAFs are the fastest growing charitable giving vehicle in the US, but more money is being put in DAFs than being granted out.[6] The chart below shows DAFs’ significant growth since 2014.

Data from NPT 2020 DAF Report[7]

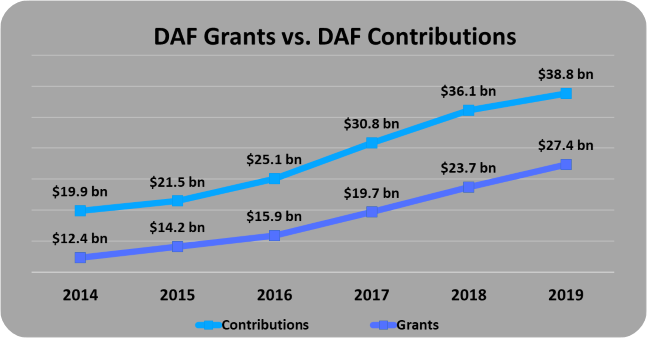

Total DAF assets have more than doubled within five years, growing at a compound annual growth rate (CAGR) of 15.17% from 2014 to 2019. The next graphic compares DAF grants (money leaving DAFs) against DAF contributions (money being put into DAFs).

Data from NPT 2020 DAF Report[8]

A clear trend is seen in the chart above: more money is being put in DAFs (contributions) than being paid out of DAFs (grants). This means that money designated to help social causes is sitting in these charitable giving accounts—now totaling $141 billion dollars. This is a major problem, and great change will be necessary to utilize these funds.

Tax Exempt Status – Regulations should limit the tax-exempt status of DAF sponsors.

Typically, DAFs come with two types of fees: an administrative fee—charged by the sponsor, and an investment fee—charged by an investment services company (remember, DAFs are not held in a simple checking account but instead are held in investment accounts to grow over time). These fees are charged annually and are a fixed percentage of the total DAF asset value (i.e., 1.5% of a $10 million donation). Because sponsors are paid a fee of the total asset value, sponsors have a financial incentive to keep money in DAFs and avoid making grants.

In 2015, Fidelity Charitable—a subsidiary of Fidelity Investments and one of the largest asset managers in the world—became the largest nonprofit in the US simply by hosting DAFs.[9] In order to establish a DAF with Fidelity Charitable, donors must agree to use investment options provided by Fidelity Investments and pay the associated investment fee. Fidelity Investments ends up profiting from its nonprofit subsidiary.

Fidelity is not the only investment services company to take advantage of DAFs. In fact, almost “every big financial services firm has set up its own charitable arm to [sponsor] DAFS” because “they [are] profit centers” from the fees they can collect.[10]

Both types of DAF fees are charged on the total assets under management (AUM), so DAF sponsors and investment services companies benefit more when DAF grants are not made. As the DAF assets grow in an investment account, so does the dollar amount of the annual fee. Sponsors’ marketing materials show saving DAFs as an underlying goal in their marketing materials, encouraging donors to “hold onto money in their account” in order to build a “legacy of giving.”[11]

Regulation should remove the tax-exempt status for nonprofit subsidiaries of investment services companies. These organizations are not actively committed to solving social problems, and a nonprofit should not exist only to earn profits for its parent company. Governments can reclaim tax revenue through this change in policy and help stop this warehousing of charitable donations.

Dormant Accounts – Regulations should implement time constraints and a dormant account program.

DAFs are frequently compared to a private foundation because the two operate in a very similar way. Ray Madoff, a professor at Boston College Law School, points out that we should actually not compare the two because “donors who put their money into advised funds receive many more tax benefits than those who give to foundations.”[12] Since the tax benefit is significantly advantageous for DAFs, the giving requirements should be stricter.

Many praise DAFs as a great tool for generational giving, but this stems from a misunderstanding of DAFs’ purpose. DAFs have no specific mission and are not designed to operate in perpetuity, like a private foundation.[13] A common suggestion to reform DAFs is to add a percentage payout requirement—similar to private foundations’ requirement of 5%—but as Chuck Collins of the Institute for Policy Studies argues, “DAF payout rates should be 100%” since DAFs’ purpose is to act as an intermediary between the donor and the receiving organization.[14] Ultimately, a payout requirement would not be effective in moving idle funds, nor is it strict enough for the tax advantages DAFs offer.

Instead, DAFs should have a five-year time constraint for grant making. This would require donors to completely distribute donations within five years or lose access to the funds. The donor has already received a tax benefit, so losing the funds would not cause a financial setback or loss. Funds remaining after five years would be flagged as “dormant accounts” and then transferred to predetermined social causes, causes that DAFs were designed to fund already. For example, dormant accounts could be used to alleviate problems in Flint, Michigan, which cost an estimated $55 million to resolve (although estimates have fluctuated), or to help those affected by natural disasters like Texas’ winter storm.[15] Dormant accounts might even go toward providing free community college, estimated to cost $9 billion per year[16]

The United Kingdom has had success with a similar initiative called the Dormant Account Scheme. The country found that hundreds of millions of pounds were sitting in inactive bank accounts, so it began channeling the funds in these accounts toward social causes. Since 2008, the Dormant Account Scheme has moved over £600 million toward disadvantaged individuals.[17]

Regulation should implement the grant-making time constraint with the dormant account program. Creating a time constraint for DAFs would ensure DAFs are being used for their intended purpose by motivating donors to make more grants or moving the funds to positive programs at the end of five years.

Foundation Donations – Regulations should eliminate foundations’ ability to donate to DAFs.

The most egregious problem with DAFs is the private foundation loophole. As mentioned previously, private foundations are required to distribute 5% of their total assets annually. Because DAFs are considered a nonprofit organization, private foundations may create a DAF and transfer funds to meet their distribution requirement. Remember that Larry Page transferred over $400 million from his foundation to meet the requirement. Instead of going to organizations in need, $400 million sits in a DAF account, growing larger and remaining idle.

Page is not the only public figure to exploit this loophole. GoPro founder Nicholas Woodman made distributions from his $500 million private foundation to the Silicon Valley Community Foundation DAF, and Elon Musk has moved at least $37.5 million from his foundation to a DAF.[18]

US regulation should eliminate private foundations’ ability to transfer funds into a DAF. To go even further, any DAF with funds from a private foundation should be required to pay out within two years of the new legislation being in place; after all, these are funds that should have been distributed already.

Conclusion – The time to make changes is now

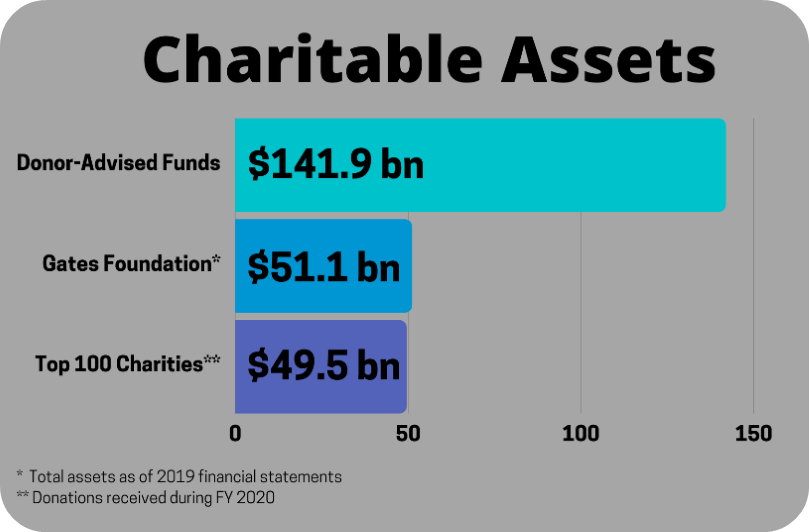

DAFs have more than enough resources to do good and solve major problems our society faces. The chart below compares DAFs with both the top 100 charities in America and the Gates Foundation, one of the largest foundations in the world.

DAFS have significantly more money than both of these combined. DAFs have the potential to help the lives of millions across the US and the world. US lawmakers have a responsibility to help unlock these unused funds for their intended use. Now is the time to stop the exploitation of DAFs and start moving the $141 billion already set aside for social good.

[1] Theodore Schleifer, “Google’s Larry Page Gave $400 Million in Christmas Donations,” Vox (2019), DOI: https://www.vox.com/recode/2019/12/18/21010108/larry-page-philanthropy-foundation-donor-advised-fund-christmas.

[2] “What Is a Donor-Advised Fund?” National Philanthropic Trust (2020), DOI: https://www.nptrust.org/what-is-a-donor-advised-fund.

[3] Julia La Roche, “Bill Ackman Donates $1.3 Billion Worth of Coupang Stock to Charity,” Yahoo Finance (2021), DOI: https://finance.yahoo.com/news/bill-ackman-donates-billion-worth-of-coupang-stock-to-charity-145442387.html

[4] “The 2020 DAF Report,” National Philanthropic Trust (2021), DOI: https://www.nptrust.org/reports/daf-report/.

[5] Will Hobson, “Zombie philanthropy: The rich have stashed billions in donor-advised charities,” Washington Post (2020), DOI: https://www.washingtonpost.com/lifestyle/style/zombie-philanthropy-the-rich-have-stashed-billions-in-donor-advised-charities–but-its-not-reaching-those-in-need/2020/06/23/6a1b397a-af3a-11ea-856d-5054296735e5_story.html.

[6] Joe Mullich, “Donor-Advised Funds: The Fastest-Growing Vehicle for Charitable Giving,” Forbes, 200, no. 5 (2017): 88.

[7] “The 2020 DAF Report,” National Philanthropic Trust (2021), DOI: https://www.nptrust.org/reports/daf-report/.

[8] Ibid.

[9] Drew Lindsay, Peter Olsen-Philips, and Eden Stiffman, “Fidelity Charitable Pushes United Way Out of Top Place,” The Chronicle of Philanthropy, 29, no. 1 (2016), DOI: https://www.philanthropy.com/article/fidelity-charitable-pushes-united-way-out-of-top-place-in-ranking-of-the-400-u-s-charities-that-raise-the-most.

[10] Marc Gunther, “America’s biggest ‘charity’ is built on a lie,” Nonprofit Chronicles (2019), DOI: https://medium.com/nonprofit-chronicles/americas-biggest-charity-is-built-on-a-lie-b6eb06295852.

[11] David Reich, “A Charitable Sleight of Hand,” Boston College Law School Magazine, 25, no. 1 (2017): 12, DOI: https://lawdigitalcommons.bc.edu/bclsm/49

[12] Ray D Madoff, “5 Myths About Payout Rules for Donor-Advised Funds,” The Chronicle of Philanthropy (2014), DOI: https://www.philanthropy.com/article/5-myths-about-payout-rules-for-donor-advised-funds/

[13] Ibid.

[14] Richard Eisenberg,, “There’s A Target on Charity’s Booming Donor-Advised Funds,” Forbes (2018), DOI: https://www.forbes.com/sites/nextavenue/2018/08/02/theres-a-target-on-charitys-booming-donor-advised-funds/?sh=1dbd57d67a32.

[15] Trent Gillies, “Flint’s crisis can be fixed with $55M in new pipes: Lansing mayor,” CNBC (2016), DOI: https://www.cnbc.com/2016/04/22/flints-crisis-can-be-fixed-with-55m-in-new-pipes-lansing-mayor.html

[16] Eugene Kiely, et al., “FactChecking Biden’s Town Hall,” FactCheck.org (2021), DOI: https://www.factcheck.org/2021/02/factchecking-bidens-town-hall-3/

[17] Commission on Dormant Assets, “Tackling Dormant Assets,” UK Government (2017), DOI: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/596228/Tackling_dormant_assets_-_recommendations_to_benefit_investors_and_society__1_.pdf

[18] Carl D Holborn and Britany Morrison, “Can Private Foundations Make ‘Qualifying Distributions’ To Donor-Advised Funds?” Taxation of Exempts, 31, no. 3 (2019): 4-6.