By Jane Robinson

Too often, the romantic sentiment of “‘Til death do us part” is being replaced with “‘Til debt do us part.”

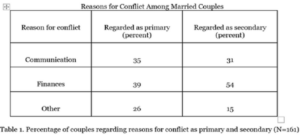

For several years, I have worked on BYU campus as a Teaching Assistant for a family finance class. Each semester, I am surprised to learn how little college students know about managing personal finances. Unfortunately, this lack of knowledge creates a problem when students get married. I have learned that financial success is directly related to marital satisfaction. Married couples tend to disagree on a variety of subjects including children, extended family, and physical intimacy; however, finances are often the biggest source of contention. Jeffrey Dew and John Dakin, family consumer science researchers from Utah State and Texas Tech Universities, conducted a two-year survey in which they followed married participants who were willing to address their emotional connection with money and the control it had on their relationship. The results of the study are shown in Figure 1.

Figure 1

Of the 161 participants surveyed, 39% stated that finances are their primary reason for conflict with their spouse, and 54% stated it as their secondary reason. Dew and Dakin propose that financial difficulties predict increased depression and higher likelihoods of divorce.2 In fact, national statistics predict that in coming years about 40% of marriages in the United States will end in divorce.3 So, with the national divorce rate increasing, struggling couples will benefit from returning to basic financial practices and positive emotional reinforcement. Specifically, I want to encourage newly-weds to spot and unearth deep-rooted financial differences before the problem grows too large to manage.

As a college student myself, I understand that students are often pressed for money. I acknowledge that some may feel uncomfortable or hesitant to talk about finances with their spouse. However, while there is no one process that’s guaranteed to benefit every couple, most financial problems in marriage can be significantly alleviated by a few practices.

Newly married (and all) couples can increase marital harmony by attempting to understand each other’s financial past, by working to set goals and follow a financial game plan, and by maintaining an open dialogue with complete transparency.

Understanding a Partner’s Financial Past

Married couples can communicate respectfully and move forward with a financial plan when they understand and accept each other’s history with money. The way a person manages their money reflects their core values and past experiences with finances. Dew and Dakin state: “Individuals connect extremely powerful meanings such as caring, security, success, and esteem to money. When spouses attach different or opposing meanings to money and its use . . . [subsequent] disagreements may have less to do with the actual financial event and more to do with the underlying meanings of money.”4

Each partner’s history with money prior to the relationship can cause differences in lifestyles and future goals. One partner might be a “saver” and has lived his or her life following a tight budget and resisting impulse buying. The other spouse might be a “spender” and is more willing to see money go. In another article, “Marriage and Finance,” Jeffrey Dew explains that although financial behaviors are a result of experience before marriage, marriage doesn’t necessarily change an individual’s relationship with money.5 When married, opposing opinions and strategies are manifest through the items that each individual believes should be incorporated into the monthly budget, what they believe they should save for versus spend money on, and where they choose to invest.

Because money management is so personal, finances should be a critical topic for couples to discuss before marriage. Daniel Matthews, a human development specialist at North Carolina University, states that “serious conflict [over money] may be avoided . . . if attitudes and philosophies about finances are clearly communicated prior to marriage.”6 However, no matter how long a couple has been together, both will benefit from having a conversation in which discrepant views are recognized and understood. The American Psychological Association (APA) suggests asking a partner the following questions to determine how they view money: “How did your family handle money growing up?” “What did your parents teach you about money?” “What are your financial goals?” “What are your fears about money?”7 So, instead of making snap judgements or belittling a spouse’s point of view, trying to understand the other’s opinions in the context of their experience with money can be more constructive. When partners make this effort, both will be more willing to compromise and discuss their financial pasts more respectfully.

Creating a Plan & Setting Goals Together

When married couples work together to create a relevant and attainable financial plan, they can come to a similar understanding about the purpose of healthy financial management.

Disagreements may have less to do with the actual financial event and more to do with the underlying meanings of money.8

Researchers in the Department of Human Development and Family Studies at Iowa State University found that the roots of financial conflict among couples are most often based on unrealistic goals and expectations and a lack of planning.9 Planning for the future (including long-term and short-term goals such as when to have children, how to save and invest, and how to build up an emergency fund), relieves unnecessary stress and brings peace of mind. Setting financial goals gives partners something concrete to work towards and to celebrate when accomplished.

After a couple has completely dissected their current financial condition, they are ready to draft a realistic financial plan. One study, published in the Journal of Family and Economic Issues, observed the financial plans of 64 self-selected couples throughout the US who believed they had great marriages. A common trait among these couples was having a primary goal to pay off debt. Over half of the couples discussed their goals to have no debt or pay off debt as quickly as possible.10

Whatever the strategy may be, all relationships will be bolstered when both partners understand and agree on an achievable financial plan. Researchers from Florida State and Jackson State Universities proposed a 5-step model for financial counselors to aid them in advising struggling couples. The steps include having the couple examine their current lifestyle, distinguish between “wants” and “needs,” establish a monthly cash flow plan, and set goals (while being flexible enough to revisit them when necessary).11 Having a plan that leads to financial stability will help relieve tension between spouses and strengthen the marriage.

Cultivating Trust and Transparency

Finally, disagreeing couples will benefit from cultivating complete financial transparency which stems from an open dialogue about their finances. According to an observational study conducted by Scott M. Stanley, co-director of the Center for Marital and Family Studies at the University of Denver, couples who cited finances as their number one topic of disagreement showed higher levels of negative interaction and tension than couples with different primary topics of conflict.12 Certainly, couples must commit to be 100% honest about spending habits and behaviors. Additionally, no matter the balance of power in managing money (maybe one spouse manages finances individually, or one manages day-to-day paying of bills and budgeting while the other controls the big-picture planning, or both spouses work in complete conjunction), each partner in a marriage should have some say in bigger decisions.

Couples who trust each other, work together as a team, and share a thorough knowledge of their financial situation are more likely to effectively manage finances, as well as other issues. When a negative event occurs, couples who have built trust and strengthened their relationship in these ways will be better equipped than those who haven’t.

Notes

1. Jeffrey Dew and John Dakin, “Financial Disagreements and Marital Conflict Tactics,” Journal of Financial Therapy 2, No. 1 (2011): 7.

2. Dew and Dakin, “Financial Disagreements and Marital Conflict Tactics,” 7.

3. Bella DePaulo, “What is the Divorce Rate, Really?” Psychology Today, last modified February 2, 2017,https://www.psychologytoday.com/us/blog/living-single/201702/what-is-the-divorce-rate-really.

4. Dew and Dakin, “Financial Disagreements and Marital Conflict Tactics,” 25.

5.. Jeffrey Dew, “Marriage and Finance,” Handbook of Consumer Science Research (2007): 337-350.

6. Daniel W. Matthews, “Marriage – A Many-Splendored, Sometimes Splintered, Thing,” The Forum for Family and Consumer Issues 1, No. 4 (1996).

7. Brad Klontz, “Money and the Family: Creating Good Financial Habits,” American Psychological Association, last modified 2015, https://www.apa.org/topics/money/family.

8. Dew and Dakin, “Financial Disagreements and Marital Conflict Tactics,” 25.

9. Cindy Fletcher, “Money Mechanics: Communication,” Iowa State University Extension (2008) https://store.extension.iastate.edu/product/4890.

10. Linda Skogrand, “Financial Management Practices of Couples with Great Marriages,” Journal of Family and Economic Issues 32, No. 1 (2011): 27-35.

11. Thomas E. Smith, “Solution-Focused Financial Therapy with Couples,” Journal of Human Behavior in the Social Environment 26, No. 5 (2016): 452-460.

12. Scott M. Stanley, “Communication, Conflict, and Commitment: Insights on the Foundations of Relationship Success from a National Survey.” Family Process 41, No. 4 (2002): 659.