By Jayson Holt

In high school, Chavonne was pushed to go to college by well-meaning friends and teachers. Although she didn’t fully understand the financial burden before her, she enrolled at the University of Mississippi. In order to pay for school, Chavonne took on $20,000 of student loans. After three semesters, she dropped out of college. She could no longer afford to attend school and pay off her debt, but her loans stuck with her. Although a college degree could help Chavonne earn more money and get out of debt sooner, returning to school was not an option for her because of her debt.[1]

Chavonne, like many other students in the United States, went to college without fully understanding what would be financially required of her. Large amounts of debt taken on at a young age can financially cripple a person for life. Financial literacy, which is defined as “an understanding of how to earn, manage, and invest money,”[2] is key to understanding debt and becoming financially secure. By being financially literate, a person can have a better understanding of how to make financial decisions. Becoming financially literate would help individuals like Chavonne to be more financially prepared to leave home.

In this article, we will explore the current state of student loans, credit card debt, and retirement in the United States. We will discuss the importance of understanding each of these topics. We will also discuss how financial education can prepare prospective and current college students to make better financial decisions and help them achieve financial security.

Student Loans

In the United States, “Total student-loan debt exceeds $1.5 trillion, surpassing both auto-loan and credit-card debt.”[3] Of the 20 million students attending colleges and universities in America, “70% will graduate with significant debt.”[4] Staggering statistics like these show that student loans are a significant part of many students’ college experiences. Such large amounts of debt stick with individuals for long periods of time.

While student loans are an obvious problem for individuals that attend college, avoiding them is not easy. In the 2017–18 school year, the average cost for an undergraduate’s tuition, room and board, and other fees at a public college in the United States was $17,797.[5] College tuition continues to go up in price, so student loans are an obvious way to fund a person’s education. Additionally, many student loans do not require payments until a person graduates from college. For these reasons, loans are an attractive option.

Although loans seem to be a good option, the average person needs 19.7 years to pay off their student debt.[6] If a person graduates from college at age 24, that person will have student debt until they are nearly 44. Their college degree, which likely took about four years to complete, will continue to be a financial burden to them for five times longer than that. For some individuals, what once seemed like a good investment has become an unreasonable option.

When deciding on which college to attend prospective college students should consider their financial situation, including any debt they may need to acquire… Community colleges are a cheaper option than larger universities, making them more appealing as far as the price an individual pays to attend.

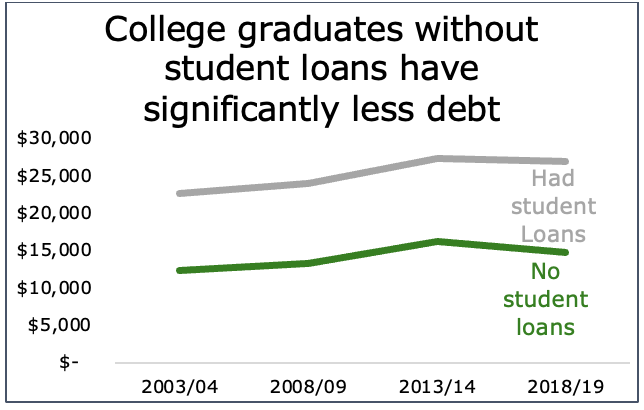

Figure 1 shows that people without student loans graduated from public universities with about half as much debt as those who had student loans.[7] Fewer student loans also mean less debt in general. Avoiding student loans helps an individual to have more financial freedom in the long run.

Figure 1

Additionally, scholarships, grants, and part-time jobs can help college students to pay for their schooling. Each of these can aid individuals to limit the number of student loans they take on to get through college. By searching online or consulting a financial advisor at the college they attend, people can better see what their financial options are.

Consumer Debt

At the end of 2019, credit card debt in the United States added up to $1.1 trillion.[8] After all, paying with a credit card is becoming increasingly common in the United States. Credit cards offer convenience to users since users don’t have to carry around physical cash or change. Additionally, credit cards enable users to buy now and pay later.

If some aren’t careful, along with student debt, credit card debt can create serious problems for them. Credit cards need to be paid off in a timely manner, or else high interest charges must be paid. If credit card charges aren’t paid off on time, a person can end up paying interest rates as high as 18.5%.[9]

Overspending can also lead to consumer debt. When college students first arrive at college, they experience an increase in personal freedom. They choose how and where to spend their money. If they aren’t disciplined, this increase in freedom can lead to consumer debt. Without a budget or some other way to track their expenditures, they will likely spend much more than they realize.

By being conscientious of and careful about how much they spend, people can avoid excessive consumer debt, especially credit card debt. By avoiding this type of debt, people can avoid high interest rates. They can keep themselves from being strapped down by continual debt payments. In summary, they can set themselves up for greater financial stability in life.

Retirement

“The Federal Reserve’s 2019 Survey of Consumer Finances found that the median person under age 55 has about $8,000 or less to retire on.”[10] This amount is tiny compared to what is actually needed. According to this statistic, retirement is not important enough to many young people. A person needs about 80% of their final working year’s salary each year thereafter to retire comfortably.[11] People need to prepare well in advance for retirement. Beginning to save for retirement at a young age can be a powerful tool for an individual.

As an example, compare a hypothetical person that began investing at age 45. If this person invested $100 per month at 6% interest (compounded annually) for 20 years, that person would have approximately $44,143 in their retirement account at retirement. If that person instead had begun investing at age 25 (assuming the interest and investment amounts remain the same), that person would have $185,714 saved up at retirement. This example illustrates the impact that starting early can have on a person’s retirement savings.

Investing for retirement can take many forms. These include (but are not limited to) traditional IRAs, Roth IRAs, and 401(k) plans. Contributions to a traditional IRA are often tax-deductible, and taxes aren’t paid on earnings until they are withdrawn at retirement. Roth IRAs are funded with after-tax money, but earnings and withdrawals are not taxed.[12] A 401(k) plan enables an employee to contribute part of their wages to different accounts.[13] By learning more about these options, people can decide how to best prepare for retirement.

Financial Education

In order to make better financial decisions, people need to gain financial education. Doing so gives individuals an understanding of how to handle their money. Individuals can gain financial education by taking advantage of learning opportunities at their college and learning on their own.

During the spring of 2019, Harvard began a workshop to teach undergraduates about personal finance. Other colleges have also begun offering similar programs.[14] Taking advantage of classes like these can help a person learn about the basics of finances. They can learn about debt, credit, retirement, and other topics.[15] Each of these topics is important for a person to understand to become financially literate. By investing time into financial education, a person can learn to make better financial decisions.

Another good option is learning individually. Books, YouTube videos, and friends or family members who understand money are all good options for gaining financial education. The hardest part is often knowing where to begin or what to learn about. As people learn, they will become increasingly confident in their financial knowledge.

Becoming financially literate is a process—for many people, a seemingly overwhelming one. When people first arrive at college, they have a lot of financial decisions right in front of them. These decisions can be extremely difficult if they have not been prepared in advance.

For students that have already been in college for some time, student loans and consumer debt may be a current reality. The best time to learn is now, and by taking steps sooner rather than later, people can get themselves in a better financial place.

Understanding student loans, consumer debt, and retirement can help students make decisions that will set them up for financial success. Each of these topics is important for individuals that want to become financially literate. By being financially educated, people can feel confident about the financial decisions they make today. As they continue to gain a financial education, they will become more competent with their money. They will set themselves up to have greater financial success in life.

Begin your financial education now. The sooner you start, the better off you will be.

[1] Elissa Nadworny and Clare Lombardo, “’I’m Drowning’: Those Hit Hardest By Student Loan Debt Never Finished College,” NPR, July 18, 2019,https://www.npr.org/2019/07/18/739451168/i-m-drowning-those-hit-hardest-by-student-loan-debt-never-finished-college.

[2] Elizabeth Coogan, “Focusing on Financial Literacy for Students,” Long Island Weekly, April 20, 2016,https://longislandweekly.com/focusing-financial-literacy-students/.

[3] Mark T. Williams, “How to Finally Address the US’s Out-of-Control Student-Loan Crisis, According to a Finance Professor,” Business Insider, March 15, 2019,http://erl.lib.byu.edu/login/?url=https://www-proquest-com.erl.lib.byu.edu/newspapers/how-finally-address-uss-out-control-student-loan/docview/2404302076/se-2?accountid=4488.

[4] Ibid.

[5] “Fast Facts: Tuition Costs of Colleges and Universities,” National Center for Education Statistics (NCES), accessed February 24, 2021, https://nces.ed.gov/fastfacts/display.asp?id=76.

[6] Williams, “Out-of-Control Student-Loan Crisis.”

[7] College Board, “Average amount of Debt per Bachelor’s Degree Recipient at Public Four-Year Colleges and Universities in the United States from 2003/04 to 2018/19 (in 2019 U.S. Dollars),” Statista, October 24, 2020, accessed February 20, 2021, https://www-statista-com.erl.lib.byu.edu/statistics/235386/us-bachelors-degree-holders-debt-levels-in-public-four-year-colleges/.

[8] Jonathan Lanning and Jonathan Rose, “United States: What are the Consequences of Missed Payments on Consumer Debts?,” Asia News Monitor, May 18, 2020, http://erl.lib.byu.edu/login/?url=https://www-proquest-com.erl.lib.byu.edu/newspapers/united-states-what-are-consequences-missed/docview/2403773485/se-2?accountid=4488.

[9] Lanning and Rose, “Consequences of Missed Payments.”

[10] Fred Makonnen, “It’s Time to Bridge the Retirement Savings Gap.” Wealth Management, October 13, 2020, http://erl.lib.byu.edu/login/?url=https://www-proquest-com.erl.lib.byu.edu/trade-journals/s-time-bridge-retirement-savings-gap/docview/2450725055/se-2?accountid=4488.

[11] Makonnen, “Retirement Savings Gap.”

[12] “Individual Retirement Accounts (IRAs),” Investor.gov, accessed February 24, 2021, https://www.investor.gov/additional-resources/retirement-toolkit/self-directed-plans-individual-retirement-accounts-iras.

[13] “401k Plans: Internal Revenue Service,” Internal Revenue Service, accessed February 24, 2021, https://www.irs.gov/retirement-plans/401k-plans.

[14] Julia Carpenter, “Even Harvard is Now Teaching Personal Finance; Professor Offering Financial-Literacy Workshops Aims to make them Relevant to Students with Diverse Economic Backgrounds,” Wall Street Journal (Online), May 18, 2019, http://erl.lib.byu.edu/login/?url=https://www-proquest-com.erl.lib.byu.edu/newspapers/even-harvard-is-now-teaching-personal-finance/docview/2226696715/se-2?accountid=4488.

[15] Carpenter,x“Professor Offering Financial-Literacy Workshops.”

Wow, great article! Thanks for the helpful information to avoid acquiring debt and how to prepare for the future.