Introduction of CDOs

Between the years 2007 and 2009, it was estimated that American households lost over $16 trillion in net worth.1 These years are widely referred to as the Great Recession, and it was the worst economic downturn that the United States had experienced since the Great Depression in the 1930s. The recession was the result of numerous problems within the US financial system that were exposed by the bursting of the housing bubble in 2006. It is impossible to place the blame on just one single factor, as there were several components that led to the downturn. However, there is one factor that seems to stand out above the rest—the widespread, irresponsible use of collateralized debt obligations within the US financial system.

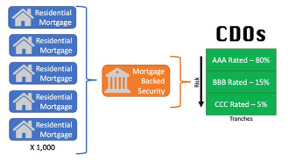

Collateralized debt obligations, otherwise known as CDOs, are a type of asset-backed security that pool a variety of different types of debt, such as mortgage-backed securities and corporate bonds. They are then split into tranches of varying levels of risk and issued to investors. The idea is that CDOs can serve as a useful financial instrument by diversifying away the risk of their underlying assets, therefore creating a safer investment opportunity. In theory, and if done correctly, CDOs should be powerful risk-management devices in our economy.2

The key phrase here is “if done correctly,” because by no means were CDOs used correctly in the years leading up to the recession. As a result, direct ties can be made between CDOs and the downfall of the US economy. Twelve years removed from the recession, one might assume that something that is considered one of the leading causes of the recession would be completely abolished from our financial system, but they would be wrong.

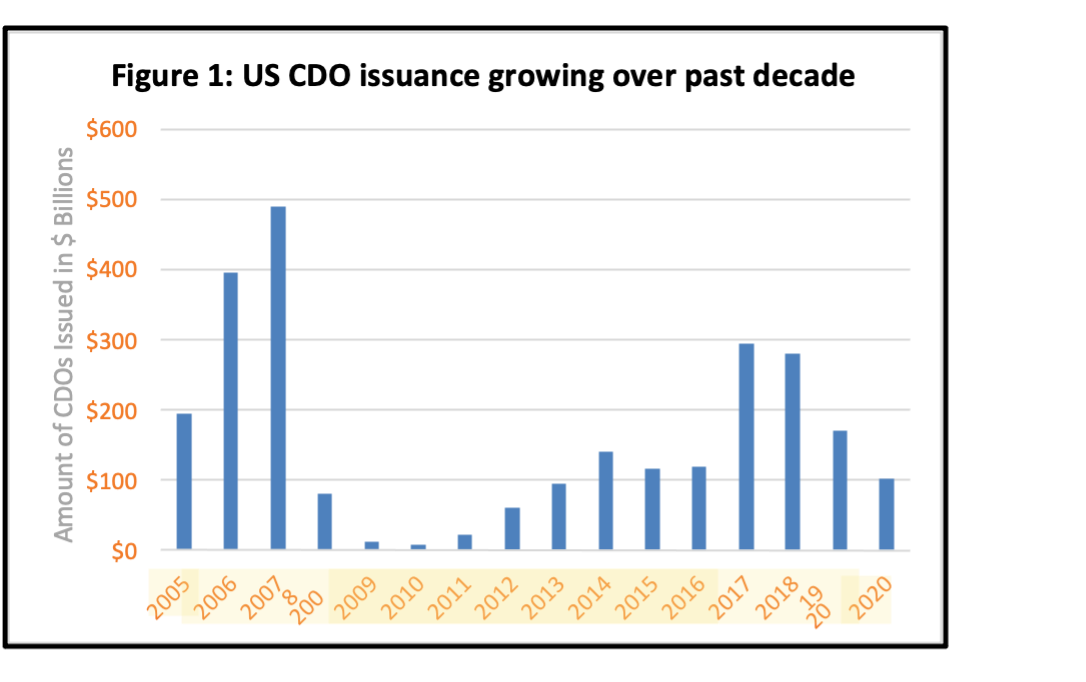

There are still billions of dollars in CDOs outstanding, with more and more being issued each year. Figure 1 shows data compiled by SIFMA, the leading trade association of the US securities industry, on annual CDO issuance in the United States.3 The graph shows that after taking a steep decline following the start of the recession, CDO issuance in the US has been gradually increasing over the past decade. The slight decline in 2019 and 2020 is due to the COVID-19 pandemic and other external factors. However, a report done by S&P Global forecasts that the issuance volume will increase to its pre-pandemic levels in 2021.4

This leads to the following question: Do CDOs have the power to send the United States into another recession? If they don’t, what has changed to allow them to be safe financial instruments in our market? To answer these questions, it is important to first look at an overview of how CDOs were handled within the US economy, and then analyze how they have changed over the last two decades. By doing this, we will be able to see that they may no longer have the same destructive power that they did in 2007.

Overview of CDOs

The first CDOs in the United States were issued by bankers at Drexel Burnham Lambert Inc. in the year 1987. Throughout the 1990s, the majority of CDOs were mainly composed of corporate bonds and consumer bank loans, and they were fairly obscure financial instruments. However, they really started gaining popularity in the early 2000s, with sales growing to around $400 billion by 2006. By this time, subprime mortgages had taken the place of consumer loans, and they made up over half of the collateral in CDOs. Between 2004 and 2007, $1.2 trillion worth of CDOs were issued within the US.5

CDOs had quickly become a large part of our financial system. Tranches of mortgage-backed securities were bundled up, and by doing so they could offer a high return while claiming to expose investors to a relatively small risk. They would then receive an undeservingly high rating, with around 80% of CDO tranches receiving a AAA rating.6 As a result, investors all over the country were buying them.

Unbeknownst at the time, CDOs were amplifying the effects of the housing bubble, which would cause major problems when it burst. Banks were originating mortgages faster than ever before; they were willing to give a mortgage to just about anyone because they knew that they would immediately be able to sell that mortgage off to a bigger bank. These bigger banks would pool together thousands of subprime mortgages into mortgage-backed securities, which would then be pooled into CDOs. In 2007, the housing bubble popped, and following a downgrade of securities, billions of dollars were instantly lost. The market for CDOs completely dried up, and the United States entered the Great Recession.

For the next few years, there were virtually no CDO sales in the US. However, over the last decade, sales in the United States have started to ramp back up. CLOs (collateralized loan obligations), which are a specific type of CDO, have been picking up a lot of steam. According to the Federal Reserve, there is nearly $600 billion of these CLOs currently outstanding.

What has changed? What makes these CDOs different from the financial instruments that destroyed our economy 14 years ago? There are a lot of differences between these CDOs and the pre-recession ones. The majority of these differences can be found by examining how issuers are handling these financial instruments now compared to how they handled them before the recession.

Change of CDOs

The problem wasn’t the CDOs themselves, but rather it was how financial institutions were packaging and selling them. CDOs were a relatively new financial instrument in the market, and as a result, investors didn’t really know what they entailed. Issuers were aware of this naivety, and they used it to take advantage of the American people.

Banks took this opportunity to create hundreds of CDOs and advertise them as low-risk investments. Banks would then sell them all off to investors, completely offloading their own risk, and therefore preventing any real consequences for themselves if the securities failed. Meanwhile, investors simply saw an opportunity to invest in something that offered them high returns while having a seemingly low risk.

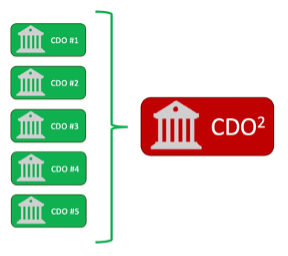

Investment banks had also begun to get creative, and they started creating even more products, such as the CDO2 and synthetic CDOs. A CDO2 is a CDO that is comprised of multiple CDOs. Synthetic CDOs are CDOs that would allow multiple bets on the same securities.

So not only were investment banks already selling these risky CDOs, but they were now creating financial instruments that were even more inauspicious. The creation of these various CDO offshoots was amplifying the magnitude of the catastrophic damage that would result from the bursting of the housing bubble. The use of CDO2s and synthetic CDOs is no longer practiced in the US financial system.

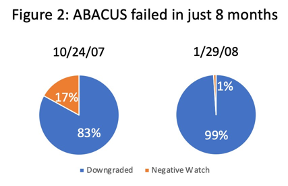

A perfect example of the moral hazard and corruption that was prevalent in our financial market prior to the recession can be found within the actions of Goldman Sachs. Goldman Sachs marketed and sold over $1 billion of a CDO known as ABACUS while failing to disclose to investors that the securities were structured by a hedge fund in such a way that they were “doomed to lose value,” 7 allowing Goldman to rake in huge profits when the securities inevitably lost their value.8

Figure 2 reflects data compiled by the SEC regarding how the makeup of ABACUS was rated at two points in time. The ABACUS deal originally closed on April 26th, 2007. As the graph shows, by October 24th, 83% of the CDO had been downgraded and 17% was on negative watch. Just 2 months later, 99% had been downgraded.9 It took ABACUS just 8 months to fail, and Goldman Sachs faced no negative repercussions because of it.

The SEC charged Goldman Sachs with fraud for their unethical actions. This set a precedent for the rest of the financial institutions in the United States that such actions would not be tolerated.

There was a multitude of underlying problems involving the use of CDOs in the United States. They were new, confusing, and unregulated; and this allowed them to wreck the economy. However, with the potential to be great investment devices, completely extirpating them from the market was not the right answer. That being said, a serious reformation was needed. The bulk of that reformation came with the introduction of the Dodd-Frank act, a set of laws that contained the most substantial changes to the US financial system since the Great Depression.

There have been many solutions aimed at solving the problems caused by CDOs. At the root of all the problems, private mortgage lending has changed drastically. Part of the Dodd-Frank act requires better disclosure from lenders on what the details of the loan entail. This is aimed at preventing homeowners from taking out mortgages that they almost certainly will end up defaulting on.

Furthermore, most of the pre-crash home loan products are gone, and now you can only choose between a fixed-rate loan or an adjustable-rate mortgage (ARM). There has also been an increase in the amount of due diligence done by lenders before issuing a mortgage, meaning that they won’t just give a mortgage to anyone that can ask for one.

At the next level, things have changed with how banks package and sell CDOs. Legislation was passed that required ABS issuers to file with the SEC, as well as disclose standardized information regarding the specific assets in each pool to both the SEC and their investors. This will prevent issuers from selling CDOs to investors without them knowing what they are buying.

Another law aimed at preventing the moral hazard involving CDOs is section 941 of the Dodd-Frank Act, otherwise known as the risk retention rule. This rule requires the securitizer of an ABS to “retain not less than 5 percent” of any ABS that they issue.10 This will prevent issuers from selling garbage CDOs, as they are required to have a stake in the security.

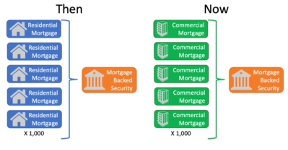

CDOs are also now being packaged with a lot more commercial mortgage-backed securities, rather than residential mortgage-backed securities because they have a much smaller default risk. But most importantly, CDOs are no longer being packaged with subprime mortgages. The American people have learned their lesson, and that is not something they want to mess with. The CDOs of today are entirely different from the CDOs of the 2000s.

Conclusion

CDOs were one of the major causes of the Great Recession for a multitude of reasons. However, despite being the reason for the biggest recession that the United States has faced in nearly a century, CDOs are still prevalent in the US financial market. This will undoubtedly lead people to wonder if these securities still have the power to send the United States spiraling into another recession. Why would we allow something to persist in our market that caused so much turmoil within our economy?

The answer is that almost everything involving CDOs is entirely different than it was in the years leading up to the recession. Kent Smetters, a professor of business economics and policy at the University of Pennsylvania, did a great job of explaining it. He said, “during the crisis, CDOs were being created for their own sake [. . .] the motivation was not risk management. Now, CDOs are more in tune with their actual purpose, which is risk diversification, not risk amplification.”11

In the years leading up to the recession, CDOs were a new concept that the world did not fully understand. Wall Street took advantage of this to create as much profit as it could while spiraling the US into a recession. It is a totally different situation now. The country is now aware of what CDOs are, how they should be used, and the damage they can cause if used irresponsibly.

With the knowledge that we as a country have gained over the past 15 years regarding CDOs, as well as the increased legislation and regulation, I do not believe that CDOs still have the power to cause another recession. Barring an absurd amount of corruption within our financial and legal systems, the likelihood that similar events happen is incredibly small. We live in a different world than we did 15 years ago, and because of this, CDOs can now be safely used as the powerful risk-management investment devices that they were designed to be, rather than catalysts for a detrimental economic downturn.

Notes

- Brian Duignan, “Great Recession,” Britannica, Last modified September 26, 2019, https://www.britannica.com/topic/great-recession

- “CDOs Are Back: Will They Lead to Another Financial Crisis?” Knowledge@Wharton, April 10, 2013, accessed December 04, 2021. https://knowledge.wharton.upenn.edu/article/cdos-are-back-willthey-lead-to-another-financial-crisis/

- “US Asset Backed Securities Statistics”, SIFMA, Last modified November 11, 2021, https://www.sifma.org/resources/research/usasset-backed-securities-statistics/us-asset-backed-securitiesstatistics-sifma/

- James Manzi, “Global Structured Finance 2021 Outlook”, S&P Global, Last modified January 8, 2021, https://www.spglobal.com/_assets/documents/ratings/research/100048329.pdf

- Duignan, “Great Recession”

- United States: FCIC, “The CDO Machine”, 127.

- Grant McCool, “Fund sues Goldman over Hudson CDO,” Last modified October 1, 2010, https://www.reuters.com/article/usgoldman-hudson-lawsuit/fund-sues-goldman-over-hudson-cdoidUSTRE6904SZ20101001

- “Amended Class Action Complaint For Violation of the Federal Securities Laws and New York Common Law,” United States District Court Southern District of New York.

- “SEC Charges Goldman Sachs with Fraud in Structuring and Marketing of CDO Tied to Subprime Mortgages,” SEC, Last modified April 16, 2010, https://www.sec.gov/news/press/2010/2010-59.htm

- “Credit Risk Retention,” Office of the Comptroller of the Currency, https://www.occ.gov/news-issuances/newsreleases/2014/nr-occ-2014-139b.pdf

- Knowledge@Wharton, “CDOs Are Back: Will They Lead to Another Financial Crisis?”