By Melissa Brown

The Backseat Girl

“Fifth place is awarded to the Backseat Girl.”

Fifth place? She had earned fourth place. On the final stretch of the race, the Backseat Girl had passed a male schoolmate who now claimed the contrary. However, it was her word against his. Even though she had crossed the finish line before him, both she and her word had lost.

I was that backseat girl. Even at a young age in an elementary school fun run, I experienced what it was like for the first time, soon-to-be many, what it was like to take the backseat to a boy.

Fast-forward from the playground to the accounting workplace. Boys in gym shorts are replaced with men in suits. Girls in sneakers are replaced with women in heels.

The gender gap is still the gender GAAP—Generally Accepted Accounting Partitions. Despite the maturity and growth expected of us when we leave the elementary school playground, gender inequality remains a present feature in everyday life. I see it in my job daily as the only female attendee in corporate finance meetings. As a woman in business, I am here to relate the facts, explain the data, and encourage action for creating a more equal accounting work environment.

THE EVIDENCE

Evidence from both the AICPA and the Financial Reporting Council show that while women have an equal presence compared to men in accounting firms upon entering the field, fewer women move upward to obtain partner positions in accounting firms.

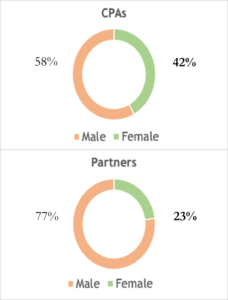

As shown in Figure 1, forty-two out of one hundred CPAs are female. At first, this number seems encouraging; however, this is only an entry-level number. The number of females who have worked up the ladder and achieved partner status is only twenty-three females out of one hundred total partners.1

Figure 1

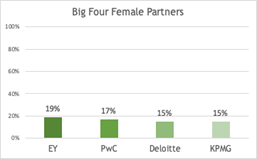

Figure 2

As shown in Figure 2, AICPA’s statistics are supported by an analysis done by the Financial Reporting Council in 2018. The council surveyed all of the Big Four companies (the leading accounting firms in the world: Deloitte, Ernst & Young [EY], PricewaterhouseCoopers [PwC], and Klynveld Peat Marwick Goerdeler [KPMG]) to determine male-to-female ratios in all positions. The research concluded that although the accounting profession has a nearly equal ratio of males to females upon entry, the number of females who have obtained a partner position beyond that compared to males is below 20 percent.2

THE EXPLANATION

So, we must ask ourselves: why does this gap exist? Two words: glass ceiling. The glass ceiling concept can be explained this way: “It is harder for women to break through that ceiling which can lead them towards the upper level of organizations—a vertical promotion.”3 The glass ceiling in the accounting work environment is the conflict between career and family goals;4 For women, the following three glass ceilings exist:

- Working long hours

- Stepping up the promotion ladder

- Accepting traditional gender roles

Working Long Hours

In the accounting profession, the workweek can consist of seventy to eighty hours during busy seasons as professionals work to finish client projects. This number of hours is considerable and easily inhibits each facet of life; specifically, family life. In other words, the accounting profession impacts the development of an individual’s different “selves,” including both professional and familial selves.

A study performed on professional and familial selves suggest that females typically have a greater desire than males to develop their parental and spousal selves, but also have a harder time doing so because of the taxing work hours required for developing their professional selves.5 The conflict between their profession and family results from the demands of the work environment. The professional self requires long hours to flourish. Working the extra time required to be successful in an accounting career is a glass ceiling that impedes women who also devote significant hours to familial development.

Stepping Up the Promotion Ladder

Working long hours is the first expectation for climbing up the career ladder; time spent working for a firm, including both total hours and longevity with the company, is the next component staff accountants need to be promoted. Because partner status is the highest level of leadership at a firm, an accountant must work long and continuous hours for upwards of thirteen to fourteen years to reach the top.6

Required longevity at a company is another example of a conflict between family and career paths, because most women need to interrupt their career at some point for maternity leave if they desire to have children. Family time is one of the top five reasons that women take a leave of absence or stop working entirely.7 When women stop working for a period to attend to family needs, they are theoretically pushed back down the promotion ladder.

The promotion ladder’s dependency on an uninterrupted career explains the gap in the number of women who achieve partner status. For example, one study revealed that only three of twenty-one female accountants had a continuous steady career path.8 Results affirm that leadership positions require time at the job. A continuous career track is a glass ceiling to females who take time off to have a family.

Accepting Traditional Gender Roles

Some women decide to continue their career paths alongside caring for children. However, it is difficult for these women to find work-family balance because society still expects women to perform motherly duties. Generally, women pursuing careers are constrained to three options:

- Leaving their jobs once they decide to have a family

- Working part-time or taking a leave of absence when a child is born

- Achieving career aspirations without a family component

Men on the other hand are allowed to pursue both a career and a family freely because that is society’s expectation. Even when women break the norm and become the family’s breadwinner, they are often being counted on to care for the children and the home.9 Traditional gender roles are being challenged, but they are still expected and difficult to change. Because gender roles are still prevalent, they inhibit women from following career aspirations.

“Traditional gender roles are being challenged, but they are still expected and difficult to change.”

Women are challenged by the gender gap to balance career and family goals in an accounting work environment. The work environment includes working long hours, stepping up the promotion ladder, and accepting traditional roles. These conflicts are three glass ceilings that stop women from progressing and explain why fewer females than males have obtained partner status in accounting firms.10

THE SOLUTION

What can companies do to help women get past this glass ceiling? The AICPA provides outlines steps for firms to implement a women’s initiative program composed by the AICPA.11 This program includes better part-time options for all employees, flexible alternatives to the ladder-up approach that change from a longevity to an effort-based approach, and ways for a firm to advocate for more female role models.

By implementing a women’s initiative program, companies can change traditional accounting work environments that have prevented women with career and family goals from progressing past the glass ceiling. Changing standards for work hour requirements and promotion guidelines in addition to fighting traditional gender roles will not only benefit women but also men who can learn from women in leadership. Women are more likely to empathize with others, inspire people to transform, and focus on self-awareness instead of self-promotion.12

As business students, we have a part to play. Women: join the gender equality army. Men: become an ally to the cause. Reducing the gender gap will make the accounting environment better, and this change begins with us.

https://www.aicpa.org/career/womenintheprofession/starting-a-womens-initiative-program.html

NOTES

- “2019 Accounting Graduates Supply and Demand Report,” American Institute of Certified Public Accountants, 2019,://www.aicpa.org/content/dam/aicpa/interestareas/accountingeducation/newsandpublications/downloadabledocuments/2019-trends-report.pdf.

- Tiron-Tudor, Adriana, and Widad A. Faragalla, “Women career paths in accounting organizations: Big4 scenario,”Administrative Sciences 8, no. 4: 62 (August 2018). https://doi.org/10.3390/admsci8040062.

- Tiron-Tudor and Faragalla, “Women career paths,” 62.

- Silva et al., “Glass Ceiling in the accounting profession: Evidence in Brazilian Companies,” Accounting and Administration 63 no. 2 (June 2018): 1–23. http://dx.doi.org/10.22201/fca.24488410e.2018.928.

- Vidwans, Mohini, and Rosemary A. Du Plessis, “Crafting careers in accounting: redefining gendered selves.”Pacific Accounting Review 32, no. 1 (January 2020): 32–53. https://doi.org/10.1108/PAR-03-2019-0027.6.

- Vidwans and Du Plessis, “Crafting careers in accounting,” 32–53.

- Vidwans, Mohini, and David A. Cohen, “Women in Accounting: Revolution, where art thou?” Accounting History, 25, no. 1 (October 2019): 89–108. https://doi.org/10.1177/1032373219873686.

- Vidwans and Cohen, “Women in Accounting,” 89–108.

- Vidwans and Cohen, “Women in Accounting,” 89–108.

- Silva et al., “Glass Ceiling,” 1–23.

- American Institute of Certified Public Accountants, “Starting a Women’s Initiative Program,” AICPA, 2017, https://www.aicpa.org/career/womenintheprofession/starting-a-womens-initiative-program.html.

- Chamorro-Premuzic, Tomas, and Cindy Gallop, “7 Leadership Lessons Men Can Learn from Women,” Harvard Business Review, April 1, 2020, https://hbr.org/2020/04/7-leadership-lessons-men-can-learn-from-women.