College students have many responsibilities and activities that require their attention, but is retirement on students’ radars? Financial planning for retirement is something that requires immediate attention. College students who have not started planning for retirement yet should take the time to learn about and actively participate in financial planning for retirement (such as using 401ks, IRAs, or both). Financial planning will allow students to take advantage of compound interest and avoid not having enough money for fun or for emergencies in retirement.

Inadequate Retirement Funds

Many people do not begin saving for retirement until later in life, and many others do not save enough. Terry Jones, an associate editor for Investor’s Business Daily, reports that “a study by the Employee Benefit Research Institute (EBRI) found that 40.6% of all households headed by someone between 35 and 64 years of age will run short of money during their retirement.”1 The sooner students begin saving, the less likely they are to be included in this humbling statistic.

Students who don’t save enough will have to pick from several options when they are older to keep their finances in check. One option is to find ways to minimize expenses, like downsizing living arrangements or refraining from traveling. Another option is to find additional sources of income after retirement besides savings, a.k.a. not fully retiring.

Sustain a Lifestyle

College students who have not begun saving for retirement need to start as soon as possible to avoid a stressful or boring retirement. Those who have retired need money to sustain their lifestyle and to do enjoyable things in retirement. To begin saving for retirement, Fidelity, a multinational financial services company, suggests knowing your retirement income replacement ratio. This ratio can be calculated by “assuming you’ll spend about 80% of the income you will be making before you retire every year in your retirement . . . for example, if your estimated preretirement income is $45,000, plan on spending about $36,000 annually in retirement.”2

This plan works well for those who like their current living arrangements and lifestyle. However, if they plan on living more expensively than they currently are, then even more money will need to be saved.

College students who do not have a full-time job can begin by estimating what their future job and income might be. Then, students can start setting aside money, even in small amounts, toward the amount of their retirement goal. Small amounts may not seem like much help toward a goal of hundreds of thousands of dollars, or even millions of dollars, but small amounts add up over time and are beneficial to savings.

Plan for Expenses

Planning to save enough for retirement to sustain a lifestyle and to be able to do many fun activities is important, but medical needs must also be budgeted into retirement savings. Many expenses can be planned out in advance, such as monthly utilities, housing, insurance, travel, and food expenses; however, medical expenses can be incurred without warning.

As bodies age, they become more susceptible to injury or disease. The Mayo Clinic (an American nonprofit academic medical center) details a few of the possible challenges that college students should expect to deal with as they become older:

- blood vessels and arteries stiffen, which increases the risk of high blood pressure and other cardiovascular problems;

- bones become weaker and more likely to fracture;

- muscles lose strength, endurance, and flexibility, which affect coordination, stability, and balance.3

These issues could lead to medical expenses for medication, physical therapy, surgery, and more.

Students need to factor in these problems that may result in unintended medical bills as they plan for retirement. Having enough money to pay for unexpected problems will prevent even more stress during already stressful situations.

Knowing the amount of money to plan for medical expenses can be difficult. Fidelity estimates that “on average a 65-year-old retired couple needs $285,000 to spend on health care over the course of retirement.”2 Figure 1, provided by Fidelity with data taken from the CEX database, shows the average medical expenses a retired couple will incur every year, depending on the couple’s age.

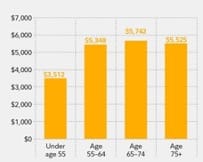

Figure 1: Average Medical Costs Per Year Per Age Group

Retired couples who are 65–74 years old spend the most, at $5,742 per year, but those who are 55–64 years old or over 75 years old are not far behind in medical expenses. Saving additional money for medical problems in retirement increases the necessary retirement amount by thousands or hundreds of thousands of dollars. However, having this money saved will enable college students to live without worry of medical bills tearing through their retirement fund.Source: Fidelity, “How much will you spend in retirement?”2 Data from CEX Database

Simple vs. Compound Interest

A very useful tool when planning for retirement is interest. Interest is the price of borrowing money. A borrower pays a lender interest for the ability to borrow money for another purpose. Two types of interest are simple interest and compound interest.

Kate Ashford, a regular contributor to Forbes Magazine, defines simple interest simply as being “calculated based only on the principal amount.”4 Simple interest is applied to the principal amount of the borrowed money, no matter the amount of interest that has already been paid.

For example, if a lender gives a $1,000 loan to a borrower for one year with a 7% annual interest rate, the borrower has to pay 0.58% on the principal amount of $1,000 each month. This monthly percentage rate comes from dividing the yearly percentage rate (7%) by the number of months in a year (12), which equals 0.58%. The lender will receive 12 payments of $5.80. The borrower will pay $70 in total interest. At the end of the year, the borrower returns the principal amount, and the lender now has $1,070.

The other form of interest is compound interest. Ashford explains that “with compound interest, you’re not just earning interest on your principal balance. Even your interest earns interest. Compound interest is when you add the earned interest back into your principal balance, which then earns you even more interest, compounding your returns.”4 Taking the same information from the previous example (a lender giving a $1,000 loan for one year to a borrower with a 7% annual interest rate), but using compound interest instead of simple interest, the interest rate per month is calculated to be 0.58%, which is the same number as in the simple interest problem.

The difference between simple and compound interest is to what the 0.58% is applied. With compound interest, the 0.58% is applied to both the principal and the previous interest payments. For the first month, the interest payment is $5.80, which is the same as with simple interest, but the second month’s interest payment is around $5.83, and the third payment is around $5.87. At the end of the year, after the borrower returns the principal amount, the lender would have $1,072.30.

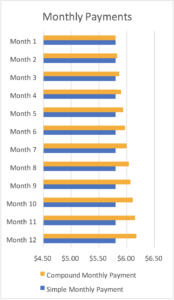

Figure 2 shows the difference in payments between the loan with simple interest and the loan with compound interest.

Figure 2: Monthly Payments for a One Year Loan of $1,000

Original Graphic

The difference between these monthly payments may not seem like a lot, but over time the results increase significantly. If the loan was over 15 years instead of 1 year, the lender would receive $1,500 in interest from simple interest versus $1,849 from compound interest. If the loan was over 30 years, simple interest would add up to $2,100, while compound interest would equal $7,116.50. Figure 3 illustrates the difference that compound interest can make over an extended period of time (based on the example of an initial $1,000 loan and a 7% interest rate).

Figure 3: Interest Earned from Simple Versus Compound Interest Investments Over Time

Original Graphic

| In both of these scenarios, the lender represents college students. Compound interest requires patience, but more importantly, compound interest requires college students to start investing early in their lives. Compound interest enables money to earn money. The longer college students put off saving, the less time they have to let savings and investments compound. In addition to foregoing free money, larger amounts of money will have to be taken out of each paycheck later in life to make up for the loss of money that could have been earned through compound interest, meaning college students will have less to live on during future stages of their lives. |

Compound Interest Methods

College students who have not started saving for retirement can begin saving by opening a 401k or IRA. A 401k is a retirement account opened by an employer for an employee that enables both the employer and employee to contribute money. An IRA is an individual retirement account that people can open for themselves.

Traditional 401ks and IRAs are contributed to with before-tax dollars. This means that money that is earned skips the tax process and goes directly into the retirement account, where the money earns interest. The Internal Revenue Service, the US federal government’s department over revenue and taxes, states that traditional 401k “distributions, including earnings, are includible in taxable income at retirement,”5 and “any deductible contributions and earnings you withdraw or that are distributed from your traditional IRA are taxable.”6 In other words, the money in traditional accounts is taxed after being withdrawn.

Another option is a Roth 401k or Roth IRA. The primary difference between Roth and traditional retirement accounts is the timing of the taxes. The IRS explains that Roth account “contributions are made with after-tax dollars,” and “withdrawals of contributions and earnings are not taxed provided it’s a qualified distribution.”7 In other words, the money in Roth accounts is taxed before being contributed to the account, where interest is earned, and then no taxes are incurred when the money is withdrawn. Either way, both traditional and Roth 401ks and IRAs enable account owners to invest their money and take advantage of compound interest.

Conclusion

For college students, the best place to start saving for retirement is by figuring out which account type works best for them. After choosing between traditional or Roth 401ks and IRAs, students need to start saving and investing money. College students should start saving for retirement now to prevent financial stress in the future. Retirement should be a time filled with fun and adventures, not filled with worry about how to pay the bills.

- Terry Jones, “Americans’ Average Retirement Savings Just Aren’t Enough—It’s Time To Change That,” Investor’s Business Daily, April 29, 2019, http://search.ebscohost.com.erl.lib .byu.edu/login.aspx?direct=true& db=buh&AN=136157711&site=eh ost-live&scope=site.

- “How Much Will You Spend inRetirement?” Fidelity, Fidelity, April 9, 2019, www.fidelity.com/viewpoints/retir ement/spending-in-retirement.

- “Aging: What to Expect,” Mayo Clinic, Mayo Foundation for Medical Education and Research, November 19, 2020, www.mayoclinic.org/healthylifestyle/healthy-aging/indepth/aging/art-20046070.

- Kate Ashford, “The Life-Changing Magic Of Compound Interest,” edited by Benjamin Curry, Forbes, Forbes Magazine, March 16, 2021. https://www.forbes.com/advisor/i nvesting/compound-interest/.

- “401k Plans: Internal Revenue Service,” Internal Revenue Service, United States Government, accessed March 21, 2021, https://www.irs.gov/retirementplans/401k-plans.

- “Traditional and Roth IRAs,” Internal Revenue Service, United States Government, March 12, 2021, https://www.irs.gov/retirementplans/traditional-and-roth-iras.

- “Roth Comparison Chart,” Internal Revenue Service. United States Government, March 11, 2021, https://www.irs.gov/retirementplans/roth-comparison-chart.