By: Zach Parrish

Famous media theorist Marshall McLuhan once said, “The more data banks record about each one of us, the less we exist.” Our privacy is seriously jeopardized, with America’s transition to a cashless society quickly accelerating. All Americans, from high school students to suburban moms, need to understand the following:

- The trend towards a cashless society in America.

- The potential impact of a cashless society on American privacy.

- Solutions that will be pivotal to preserving our privacy.

What’s With the Current Trend?

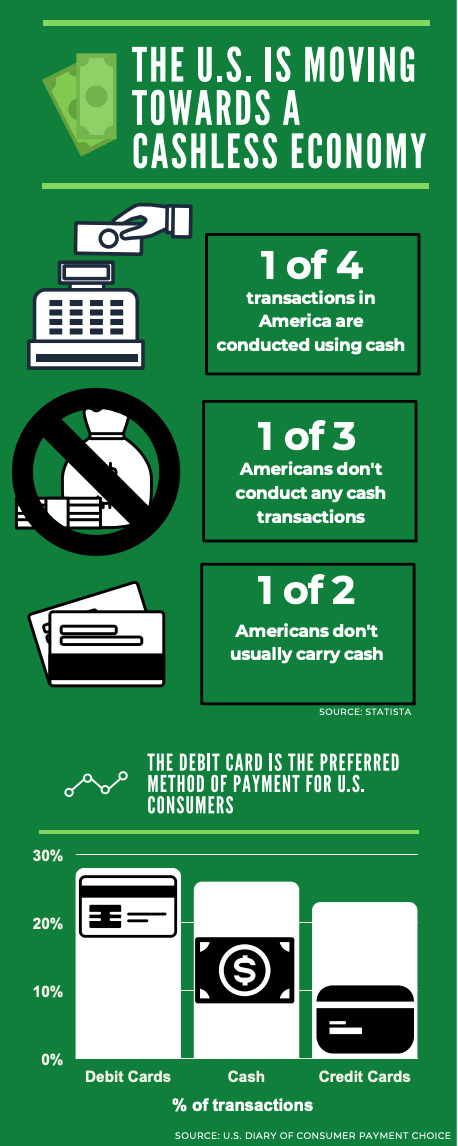

America is quickly moving to a cashless society. Figure 1 shows that Americans use cash in only one of every four transactions, and the debit card has overtaken cash as the preferred payment method for U.S. Consumers. According to the American Institute of Economic Research, only 7% of money circulated in America is represented in bills and coinage. COVID-19 has only accelerated this trend. Cash withdrawals from ATMs plunged 25% nationwide during the pandemic, and the number of Americans using person-to-person transfer services such as Venmo increased by 43% in 2020. One economist described COVID-19’s impact on the payment system as compressing a number of years of growth in cashless payments into a number of months. This trend toward going cashless is expected to continue after COVID-19. Some Americans have raised concerns that our country will soon abandon cash altogether.

Businesses also drive the trend towards a cashless society. In the past year, many companies have transitioned away from cash. Consumers across the country have stood in line at cashless stores only to realize that money – legal tender for all debts, public and private – is not accepted. Other stores, such as the new Amazon Go store, are entirely cashier-less, eliminating customers’ ability to pay with cash. The power of businesses to restrict cash as a payment type has been hotly debated. While legislation to address this issue is pending, the debate rages on.

Impact

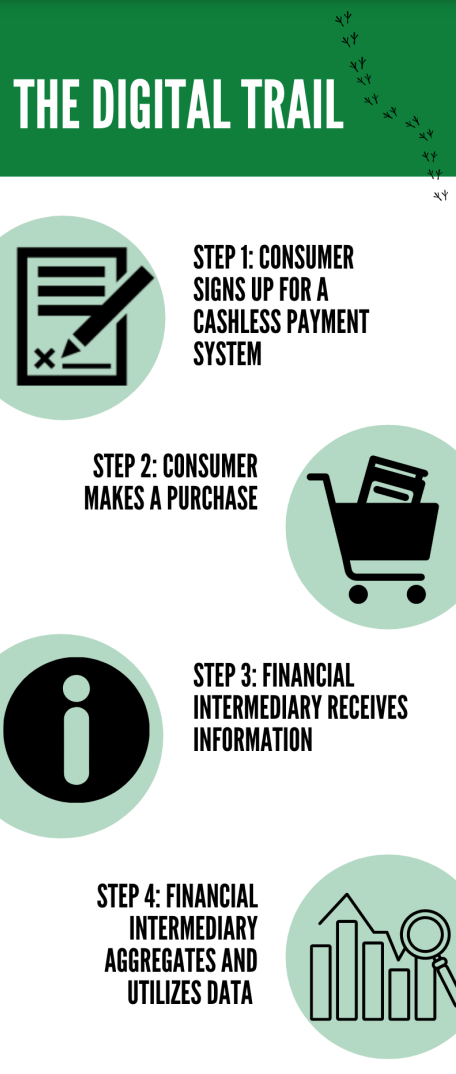

We must understand how digital transactions are processed to appreciate the consequences of a cashless economy on American privacy. Each time a transaction takes place, a financial intermediary receives an electronic transaction record. Over time, the financial intermediaries aggregate this data. The data can then be sorted by individual, revealing not only an individual’s consumer preferences but also sensitive personal information such as health status and financial ability. The data can then be sold to other businesses or the government. By purchasing this data, an insurance company could obtain, for example, access to a consumer’s food purchases or frequency of gym attendance, and the government could track the location of its citizens.

Governments and businesses are willing to pay large sums to access this valuable data. They are incentivized to push America towards a cashless economy. As Forbes’ Frank Sorrentino said, “When an economy goes cashless, consumers no longer have the right to choose whether or not to remain anonymous.” This lack of anonymity is of particular concern because many financial intermediaries and other companies spearheading the movement to a cashless economy are technology companies that fall outside the current regulatory framework, further putting our consumer privacy at risk. These institutions and perverse incentives can potentially destroy our privacy without serious reform.

America is not yet a cashless society, but our privacy is invaded daily by institutions that aggregate consumer data. Target, the U.S. grocery retailer, made national news when a father found out his high school daughter was pregnant through targeted ads from Target. Using a cashless payment form to purchase pregnancy-related items, the teenage girl allowed Target to share her most sensitive private information. To financial intermediaries, it’s all about the revenue available from selling their data to other companies or the government, which can use that data to further their objectives. And none of the players is incentivized to consider the interests of the consumers whose data they obtain.

We can see a glimpse of our future as a cashless society by looking at the example of the People’s Republic of China. China, one of the world leaders in transitioning to a cashless economy, is implementing a “social credit system.” Consumer data generated by electronic transactions is combined with other data obtained by the Chinese government to create a score to measure an individual’s behavior and trustworthiness. The foundation of the social credit system is the government’s ability to track the financial transactions of each of its citizens. After utilizing cashless transactions to gather data, the Chinese government can use the score to punish or reward its citizens. Those who don’t measure up may forfeit the ability, for example, to book a flight, buy property, or take out a loan. And like something out of a dystopian novel, individual citizens can do little to change their scores based on massive amounts of aggregated data. With no algorithmic transparency about how that data is used to generate a citizen’s social credit score, Chinese citizens are largely unable to challenge their scores. Though an extreme example, the Republic of China should serve as a cautionary tale for our country.

Solutions

While America’s transition to a cashless society is accelerating, we must take three steps to preserve American privacy:

- Cash must be preserved as a form of payment for U.S. citizens. Groups such as the Consumer Choice in Payment Coalition (CCPC) are working with legislators to ensure that cash will remain an available form of payment in the United States.

- The United States Congress must pass legislation to restrict the acquisition and use of our personal data by both private and government interests. Our data in the hands of the government is a temptation for tyrants.

- We must reform the federal regulatory system to include the oversight of all entities that act as financial intermediaries in cashless transactions so that we can limit how the data they collect can be sold or used to violate our privacy. While America will continue its transition to a cashless society, these measures will provide some hope of protecting American privacy and ensuring that consumers can remain anonymous.

Looking Ahead

The trend towards a cashless society will be around for a while. It’s only going to accelerate. And the impact of America’s transition to a cashless economy will be catastrophic. The future of our right to privacy hangs in the balance. As citizens of the United States, we have the opportunity and responsibility to stand up and defend that right. Decide now to use cash and vote to overhaul the current regulatory framework to limit government access to your transaction history. The protection of your privacy depends on it.

Notes

i “Marshall McLuhan Quotes.” AZ Quotes. Accessed March 15, 2021. https://www.azquotes.com/quote/195308

ii Kumar, Raynil, and Shaun O’Brien. “2019 Findings from the Diary of Consumer Payment Choice.” Federal Reserve Bank of San Francisco. Federal Reserve Bank of San Francisco, June 26, 2019. https://www.frbsf.org/cash/publications/fednotes/2019/june/2019-findings-from-the-diary-ofconsumer-payment-choice/.

iii “U.S. Cash in Circulation.” AIER, January 28, 2021. https://www.aier.org/.

iv Maykuth, A. (2020, Jul 06). How COVID-19 is accelerating the shift to a cashless society. TCA Regional News Retrieved from http://erl.lib.byu.edu/login/?url=https://wwwproquest-com.erl.lib.byu.edu/wire-feeds/how-covid19-is-accelerating-shiftcashless/docview/2420047179/se2?accountid=4488

v Yerkes, M. (2020). Are we becoming a cashless society? Independent Banker, 70(11), 62-67. Retrieved from http://erl.lib.byu.edu/login/?url=https://wwwproquest-com.erl.lib.byu.edu/trade-journals/are-webecoming-cashless-society/docview/2458778968/se2?accountid=4488

vi Yerkes, M. (2020). Are we becoming a cashless society? Independent Banker, 70(11), 62-67. Retrieved from http://erl.lib.byu.edu/login/?url=https://wwwproquest-com.erl.lib.byu.edu/trade-journals/are-webecoming-cashless-society/docview/2458778968/se2?accountid=4488

vii Selyukh, Alina. “Cities and States Are Saying No To Cashless Shops.” NPR. NPR, February 6, 2020. https://www.npr.org/2020/02/06/803003343/some-businesses-are-going-cashless-but-cities-arepushing-back.

viii Fourtane, Susan. “Sweden. World’s First Cashless Society. Interesting Engineering. December 24, 2020. https://interestingengineering.com/sweden-how-tolive-in-the-worlds-first-cashless-society

ix Sorrentino, Frank. “The Debate Over A Cashless Economy.” Forbes. Forbes Magazine, January 11, 2021. https://www.forbes.com/sites/franksorrentino/2019/08/29/the-debate-over-a-cashless-economy/.

x Purewal SJ. The privacy and security implications of a cashless society. PC World. 2013;31(1):33-34. https://jespublication.com/upload/2022-V13I7155.pdf

xi Sorrentino, Frank. “The Debate Over A Cashless Economy.” Forbes. Forbes Magazine, January 11, 2021.

xii “United States: The Digitalization of Payments and Currency: Some Issues for Consideration – Governor Lael Brainard.” Asia News Monitor, February 10, 2020.

xiii Hill, Kashmir. “How Target Figured Out A Teen Girl Was Pregnant Before Her Father Did.” Forbes. Forbes Magazine, March 31, 2016. https://forbes.com/sites/kashmirhill/2012/02/16/how-target-figured-out-a-teen-girl-was-pregnantbefore-her-father-did/?sh=193c40e96668

xiv Kobie, Nicole. “The Complicated Truth about China’s Social Credit System.” WIRED UK. WIRED UK, June 7, 2019. https://www.wired.co.uk/article/china-social-creditsystem-explained.

xv “Cash Choice: Consumer Choice in Payment Coalition.” Consumer Choice in Payment Coalition. CCPC, 2021. https://www.cash-choice.org/.

xvi “Cashless Society Is a Temptation for Tyrants.” The Wall Street Journal, August 10, 2016. https://www.wsj.com/articles/cashless-society-is-atemptation-for-tyrants-1470861156.