Have you ever wanted to start your own business? Most people haven’t. Starting a business sounds like a logistical and costly nightmare; however, a properly managed startup can reap great rewards. Forbes magazine reported on March 17th, 2020 that Bill Gates has a net worth of 99.3 billion from Microsoft: a startup company that grew into one of the most successful global businesses in the world.[1] Building a successful startup, like Microsoft, can be broken down into three main steps: planning, finding funding, and working out logistics.

Planning

The first step for building a successful business is making a plan. Planning for a business involves three key elements:

- Product or service development

- Market research

- Pricing/cost analysis

Business planning begins with an idea for a product or service. Great startups find products or services that solve a relevant problem, or pain point, for their customers. For example, when touch screens became popular, the glove company Agloves noticed that smartphone users had to take off their gloves in the cold to use touch screens. To capitalize on this user issue, Agloves developed touchscreen-sensitive gloves to solve that problem.[2]

When considering product ideas for a startup, you need to consider the pain point that it could solve. Ask yourself: what problem would my product or service be solving? How significant is this problem? How much would I pay for a solution to this problem?

The target market for a startup is the people who experience that pain point. For example, Agloves targeted the market of people who were touchscreen users. Indeed, for a business to succeed, they must have a market large enough to sustain profitability. Figure 1 shows the top six reasons for startup failure; the number-one reason listed is that there was no market needed for the startup’s product or service. Remarkably, 42% of startup failures reported no market needed as a reason for startup failure, whereas only 17% of those same companies reported having a poor product as a reason for failure. In other words, having a market for a product is even more important to a business’s success than the quality of its product.

In addition to market research, businesses must also set the right price for their product. Startup companies often struggle to price their products correctly, because they need to price their product high enough to gain a profit, but low enough to make enough sales. Some helpful strategies to set the right price include:

- Asking focus groups how much they would pay for a product

- Comparing prices with similar existing products

While pricing a product, startup companies need to know how much making and delivering the product will cost. For example, if someone wanted to start a hamburger restaurant, they must obtain accurate cost estimates to find out how much each hamburger will cost to make. Those cost estimates should include the cost of the food, labor, and any other costs directly associated with making that product and giving it to the customer.

When performing cost analysis, startup companies also need to consider overhead costs: the costs associated with rent, utilities, and any other indirect costs that they must pay to maintain the business. One helpful cost analysis is a break-even analysis—a simple arithmetic function that allows for a business to understand how much of a product they must sell at a certain price to avoid a financial loss.

In summary, a well-planned startup company must develop a product or service that solves consumer problems and ensure that a sustainable market exists for their product, and carefully set a price for their product.

Funding

Looking back to Figure 1, the second most prevalent reason for startup failure is a lack of funding (that is—they ran out of cash). Most startup companies aren’t very profitable at first, so finding funding is an important step to getting a business going. As one development company has said, startups can be funded from bootstrapping, loans, angel investors, venture capital, crowdfunding, startup accelerators, and local economic development organizations.[4] Each source of funding could work for different situations, making it imperative to have a business plan before deciding on which kinds of funding to pursue.

In almost all sources of funding, startup businesses must persuade others to invest in their company. Dutta Baishakhi, the Senior Assistant Editor for The Economic Times, suggests the following strategy for a startup company to woo their potential investors:[5]

- Have a clear go-to-market strategy

- Be able to explain the problem they want to address, why it persists, and how their solution will solve it

- Demonstrate confidence and persuasiveness through a well-rehearsed presentation

- Validate the benefits their solution can provide over the competition

If a startup company has already developed an idea for a product that addresses a relevant problem, and has a market, their next steps are creating a persuasive presentation and demonstrating how they can provide benefits over their competitors. In other words, a lot of the work for finding funding should be completed in the early stages of business planning if the startup has a good product and an available market. With that in mind, creating a persuasive presentation should be simple if the product really does address a relevant problem for an available market. However, validating the benefits a startup can provide over their competition can prove to be more difficult. A healthy understanding potential competition is thereby important for developing a stand-out marketing plan; thus, thorough research of competitors is a necessary part of market research.

To recap, startups need funding to succeed. Startups must choose the best source of funding for their company and persuade investors to invest in them. However, even once a startup has a plan and funding, it’s not quite ready to launch yet. There’s one more critical step: logistics.

Logistics

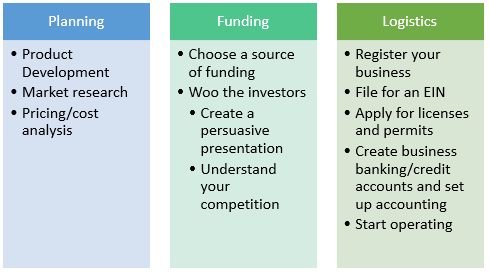

Without a good logistical setup, even the most promising of startups can falter and fail. Cara MacDonald, a writer for KSL.com, wrote an article with helpful steps to complete all of the logistical necessities.[6] These steps are summarized in Figure 3.

These logistical steps begin with registering the business. To do so, the startup company must first choose a business structure. The startup can choose to register as a corporation, nonprofit corporation, Limited Liability Company, Sole Proprietorship, General Partnership, Limited Partnership, Limited Liability Partnership, or a Collection Agency.6 Next, the company must file for an Employer Identification Number (EIN). This number is an identification number for businesses and is necessary for filing taxes. After that, the company must apply for any necessary licenses and/or permits. Once these permits are acquired, the company must create business banking and credit accounts (and set up their accounting department). Additionally, in the article about the logistics of starting a business, MacDonald listed the following as important steps for beginning operation:

- Obtain business insurance

- Define your brand

- Establish a web presence

- Hire employees

- Buy assets and equipment

- Execute your marketing plan

- Prepare for emergencies

MacDonald also noted that, for Utah business orders, Utah.gov is a great resource to reference in order to make sure the startup remains legally compliant. While of course some businesses require more complex steps in the logistical department, these are the basics.

Conclusion

Starting a business appears daunting, but it is much more manageable if prospective business owners break down the process and take it one step at a time. Planning, finding funding, and working out logistics are all necessary steps for a company to startup smoothly. Every startup is unique and will face unique challenges, but generally, each startup will need to work through the steps summarized in Figure 3.

Entrepreneurs must understand that it is critical to study their target markets and make sure that a large enough market exists for their intended product or service, otherwise, their business will fail. However, following the steps of great planning, securing funding, and working through each logistical step will help a startup business build a sturdy foundation and prepare for success.

Last Updated: 8/28/20

[1] “Bill Gates.” Forbes. Forbes Magazine. Accessed March 17, 2020. https://www.forbes.com/profile/bill-gates/#177ceb2689f0.

[2] Ellevate. “From Cold Hands to Hot Sales.” Forbes. Forbes Magazine, February 8, 2012. https://www.forbes.com/sites/85broads/2012/02/07/from-cold-hands-to-hot-sales/#52c59a23b997.

[3] McCarthy, Niall. “The Top Reasons Startups Fail [Infographic].” Forbes. Forbes Magazine, November 3, 2017. https://www.forbes.com/sites/niallmccarthy/2017/11/03/the-top-reasons-startups-fail-infographic/#60eefe724b0d.

[4] Needham, Alison. “Show Me the Money: 6 Ways to Finance Your Startup.” Home – Santa Clarita Valley Economic Development Corporation. Accessed February 29, 2020. https://www.scvedc.org/blog/show-me-the-money-6-ways-to-finance-your-startup

[5] Dutta, Baishakhi. 2019. “Inside the Investors’ Mind – how to Get Your Startup Funded!” Electronics Bazaar, Apr 22. https://search.proquest.com/docview/2211934349?accountid=4488

[6] MacDonald, Cara. 2019. “Starting a Business in Utah for the Absolute Beginner.” KSL.Com, Apr 20. https://search.proquest.com/docview/2211573501?accountid=4488